The Hidden Risk of "Saving": Why Your Bank Account is Losing Value Every Year

A must-read for every hard-working Nepali family.

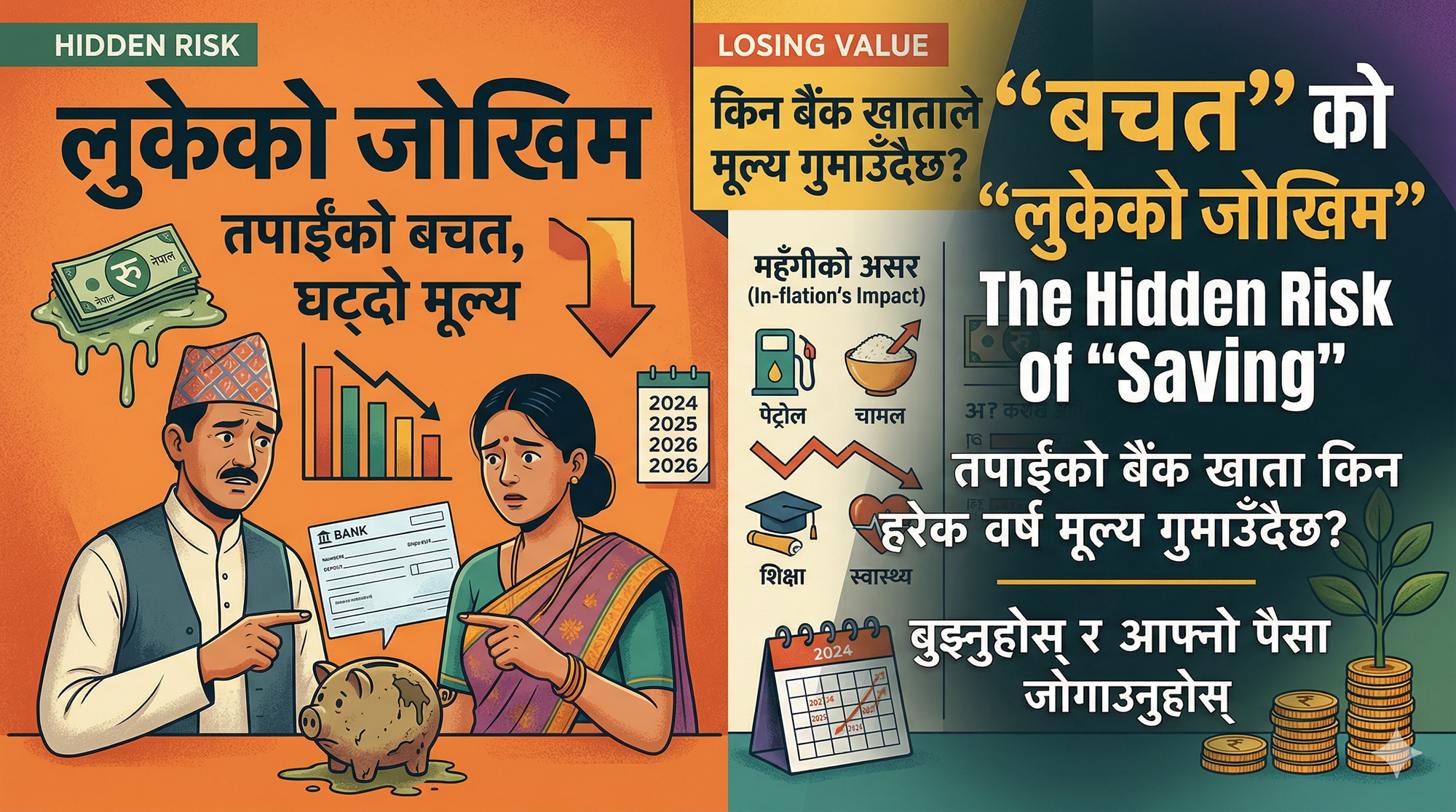

If you are a lower-middle-class Nepali today, you likely work very hard to set aside a portion of your monthly income. You might be keeping it in a "Bachat Khata" (Savings Account) at a commercial bank, thinking your money is safe and growing.

But here is the hard truth: If your money is just sitting in a regular savings account, you are actually becoming poorer every day.

1. The Simple Math Banks Don't Highlight

As of April 2026, the annual inflation rate in Nepal is roughly 3.62%. This means a basket of goods (vegetables, ghee, school fees) that cost NPR 1,000 last year now costs about NPR 1,036.

Meanwhile, most regular savings accounts in Nepal are offering interest rates between 2.75% and 3.0%.

| Category | Rate (%) |

|---|---|

| Average Inflation (Price Rise) | 3.62% |

| Average Bank Interest (Growth) | ~2.85% |

| Net Yearly Loss in Value | -0.77% |

*Your bank balance might look higher on your app, but the purchasing power—what that money can actually buy—is shrinking.*

2. The "Milk and Petrol" Reality

Lower-middle-class families feel inflation most in daily essentials. In the last year alone:

- Vegetables: Prices have seen hikes of over 11%.

- Education: School fees and materials have risen by nearly 7.5%.

- Ghee and Oil: Prices have increased by nearly 9.8%.

If you saved money for your child’s college or a new plot of land, and that money grew at only 3% in a bank, you are now further away from those goals than you were a year ago.

3. The Psychology of the "Safety Trap"

In Nepal, we are culturally taught that "Saving is Virtue." We trust the bank because the building is big and the passbook feels real. However, "Saving" is not the same as "Investing."

Saving is for Emergencies

Keep 3–6 months of expenses in a bank for immediate needs (health, job loss).

Investing is for Wealth

Put money where it grows faster than the price of milk, petrol, and land.

4. What Should You Do Instead?

To stop your money from melting away, consider these common alternatives available in Nepal:

- Fixed Deposits (Muddati Khata): While regular savings offer ~2.8%, Fixed Deposits for 3 years or more can offer 4.5% to 5.5%. This is the simplest way to stay above inflation.

- Debentures: Many Nepali banks issue debentures that pay 8% to 9% interest. These are generally safe and offer much higher returns than a savings account.

- Mutual Funds (SIP): For those who fear the stock market, Systematic Investment Plans (SIPs) allow you to invest as little as NPR 1,000 a month. Professional managers handle the risks for you.