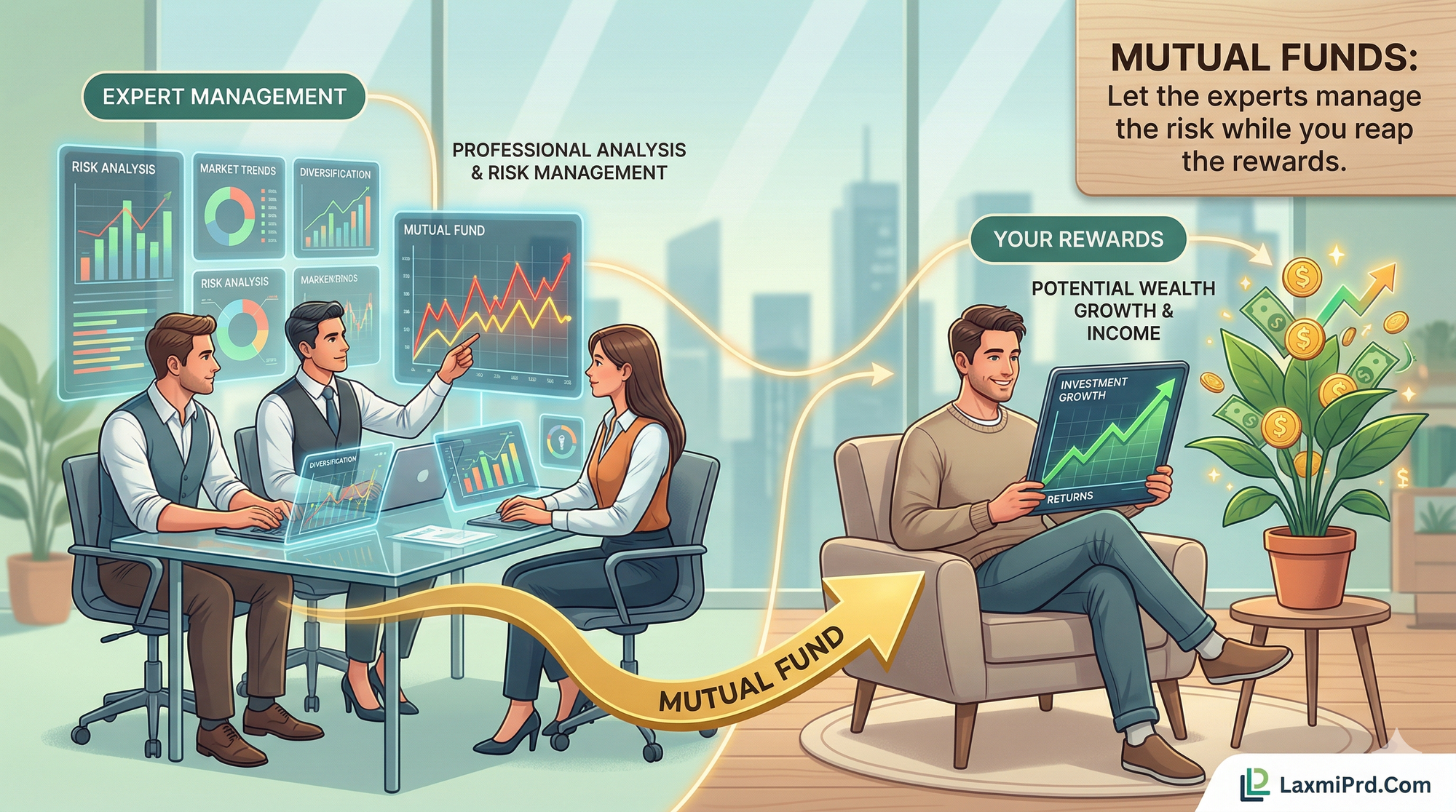

Mutual Funds: Let the experts manage the risk while you reap the rewards.

Why Nepali investors are discovering that professional fund managers beat DIY stock picking—and how to choose between open-ended flexibility and closed-ended discipline.

The Microbus vs. The Tourist Bus

Imagine you're traveling from Kathmandu to Pokhara. You have two options. Option one: a crowded microbus where you squeeze between strangers, the driver takes dangerous shortcuts, and you constantly worry about breakdowns. Option two: a tourist bus with a professional driver, scheduled stops, and maintenance checks. Both get you to Pokhara, but which journey would you prefer?

This is the difference between DIY stock investing and mutual funds. When you buy individual shares, you're the microbus passenger—exposed to every bump, every reckless turn, every mechanical failure. When you invest in a mutual fund, you're on the tourist bus with a professional fund manager navigating the NEPSE highway while you sit back and enjoy the scenery. The volatility is the same; your experience of it is completely different.

For lower-middle-class Nepali families who lack the time to research companies, track quarterly reports, or analyze market trends, mutual funds offer something precious: peace of mind with profit potential.

Understanding the Two Types: Open-Ended vs. Closed-Ended

Before you invest, you need to understand the two distinct flavors of mutual funds available in Nepal. Each serves different financial goals and timelines.

Open-Ended Mutual Funds: The Flexible Friend

Open-ended funds work like a digital wallet for investments. You can buy units (join the fund) or sell units (exit the fund) on any business day at the current Net Asset Value (NAV). The fund continuously issues new units to incoming investors and redeems units from those leaving. There is no fixed maturity date.

Key characteristics:

- Liquidity: Buy or sell any time during market hours

- Price: Determined daily based on NAV (total fund value divided by units outstanding)

- Minimum investment: Often as low as NPR 1,000–5,000

- Exit load: Some funds charge 1–2% if you exit within 6–12 months

Closed-Ended Mutual Funds: The Disciplined Saver

Closed-ended funds operate like a fixed-term savings scheme with stock market returns. The fund raises capital during an Initial Public Offering (IPO) phase, then closes to new entries. Your money stays invested for a fixed period—typically 5–7 years—after which the fund matures and returns capital plus gains. During this period, you can only exit by selling your units on the secondary market (like NEPSE shares) if buyers exist.

Key characteristics:

- Fixed tenure: Typically 5–7 years from launch date

- Entry: Only during IPO phase or secondary market purchase

- Exit: At maturity, or by selling units on NEPSE if liquidity exists

- Discount opportunity: Often trades below NAV in secondary market, offering value entry points

Expected Outcomes and Timelines: What the Numbers Show

Let's talk about realistic expectations. Mutual funds in Nepal don't promise guaranteed returns (SEBON regulations prohibit this), but historical data provides guidance.

| Fund Type | Minimum Recommended Timeline | Historical Return Range (Annualized) | Best For |

|---|---|---|---|

| Open-Ended Equity Fund | 3–5 years minimum | 10%–18% (varies with NEPSE cycles) | Flexible goals, emergency access |

| Open-Ended Debt/Bond Fund | 1–3 years | 6%–10% (lower volatility) | Conservative investors, short-term goals |

| Closed-Ended Fund (IPO Entry) | 5–7 years (fixed maturity) | 12%–20% (potential for higher returns due to locked-in capital) | Long-term wealth building, discipline enforcement |

| Closed-Ended Fund (Secondary Market) | Until maturity (2–6 years remaining) | Variable; discount purchases can yield 15%–25% | Value investors seeking discounts |

These returns significantly outperform savings accounts that lose value to inflation, though they come with market volatility that requires patience to navigate.

Why Professionals Beat DIY Investing

The fund manager's job is to wake up every morning thinking about the market. They have research teams, access to company management, Bloomberg terminals, and years of experience reading balance sheets. You have a day job, family responsibilities, and perhaps two hours on Sunday to check your portfolio.

Professional advantages include:

- Diversification: A single equity fund might hold 20–40 different stocks across sectors. You'd need lakhs of rupees to replicate this individually.

- Risk Management: Fund managers can hedge positions, hold cash during downturns, and rebalance strategically.

- Emotional Discipline: They don't panic sell when NEPSE drops 200 points because they understand volatility is not loss.

- Regulatory Oversight: SEBON regulates fund operations, ensuring transparency and preventing fraud.

For a lower-middle-class investor earning NPR 40,000–60,000 monthly, mutual funds democratize access to professional wealth management that was once reserved for the elite.

The SIP Strategy: Small Drops Fill the Ocean

Systematic Investment Plans (SIPs) are the secret weapon for Nepali families with limited lump-sum capital. Instead of needing NPR 100,000 to start, you commit to investing NPR 1,000, NPR 5,000, or NPR 10,000 every month automatically.

The magic of SIPs works in two ways. First, rupee cost averaging: When NEPSE is high, your fixed amount buys fewer units. When NEPSE crashes, the same amount buys more units. Over time, your average cost per unit smooths out market volatility. Second, psychological ease: You don't need to time the market or make decisions every month. The automation builds discipline that most DIY investors lack.

Consider this realistic scenario: A teacher in Birgunj starts a SIP of NPR 5,000 monthly in an open-ended equity fund. Over 5 years (60 months), she invests NPR 300,000 total. Assuming a conservative 12% annualized return, her corpus grows to approximately NPR 400,000–420,000. The NPR 100,000+ "profit" comes from consistent participation, not market timing genius.

Choosing Your Fund: Practical Guidelines

With dozens of mutual funds now operating in Nepal, selection matters. Here's how to evaluate:

1. Check the Fund Manager's Track Record — Look at 3–5 year historical performance. Past returns don't guarantee future results, but consistent underperformance relative to peers signals poor management.

2. Understand the Expense Ratio — This is the annual fee deducted from your returns (typically 1.5%–2.5% in Nepal). Lower is better, but don't sacrifice quality management for a 0.5% fee difference.

3. Match the Fund Type to Your Goal — Saving for a child's education in 10 years? Closed-ended equity fund or long-term open-ended equity. Building an emergency corpus? Open-ended debt fund with instant redemption.

4. Verify SEBON Registration — Only invest in funds licensed by the Securities Board of Nepal. Unregistered schemes promising guaranteed high returns are scams.

The 2026 Landscape: Digital Access and Rural Reach

The mutual fund ecosystem in Nepal has transformed dramatically. What once required visiting fund offices in Kathmandu is now accessible via mobile apps and bank branches in district headquarters. Digital literacy initiatives are bringing financial tools to populations previously excluded from formal investing.

Major commercial banks now offer "fund supermarkets" where you can compare and invest in multiple schemes through your existing bank account. The Nagarik App and national digital infrastructure are streamlining KYC processes, making it easier for every Nepali citizen to open investment accounts.

For lower-middle-class families in places like Nepalgunj, Butwal, or Surkhet, this means professional wealth management is no longer a Kathmandu privilege. It's a national opportunity.

The Timeline Reality: When Will You See Results?

Impatience destroys mutual fund returns. Many Nepali investors check their NAV daily, panic at monthly declines, and exit within six months—locking in losses and missing the recovery.

Here's what to expect:

- 0–6 months: Your returns will likely be negative or flat. Markets fluctuate; short-term noise dominates.

- 6 months–2 years: You may see 5%–15% gains, but volatility will be high. One quarter might show 20% returns; the next might show -10%.

- 3–5 years: The trend becomes clearer. Quality equity funds typically show 10%–15% annualized returns, compounding into meaningful wealth.

- 5+ years: The magic of compounding becomes visible. Your initial investment has potentially doubled, and the corpus generates significant passive income through dividends.

If you cannot commit to at least 3 years for equity funds, you should not invest in them. Use debt funds or fixed deposits instead. Time in the market beats timing the market—always.